Payday loans are legal in most states, but illegal or capped at very low rates in about 21 states and the District of Columbia.

If your state allows them, a storefront or online lender can put a few hundred dollars in your hand today. The trouble shows up in two weeks.

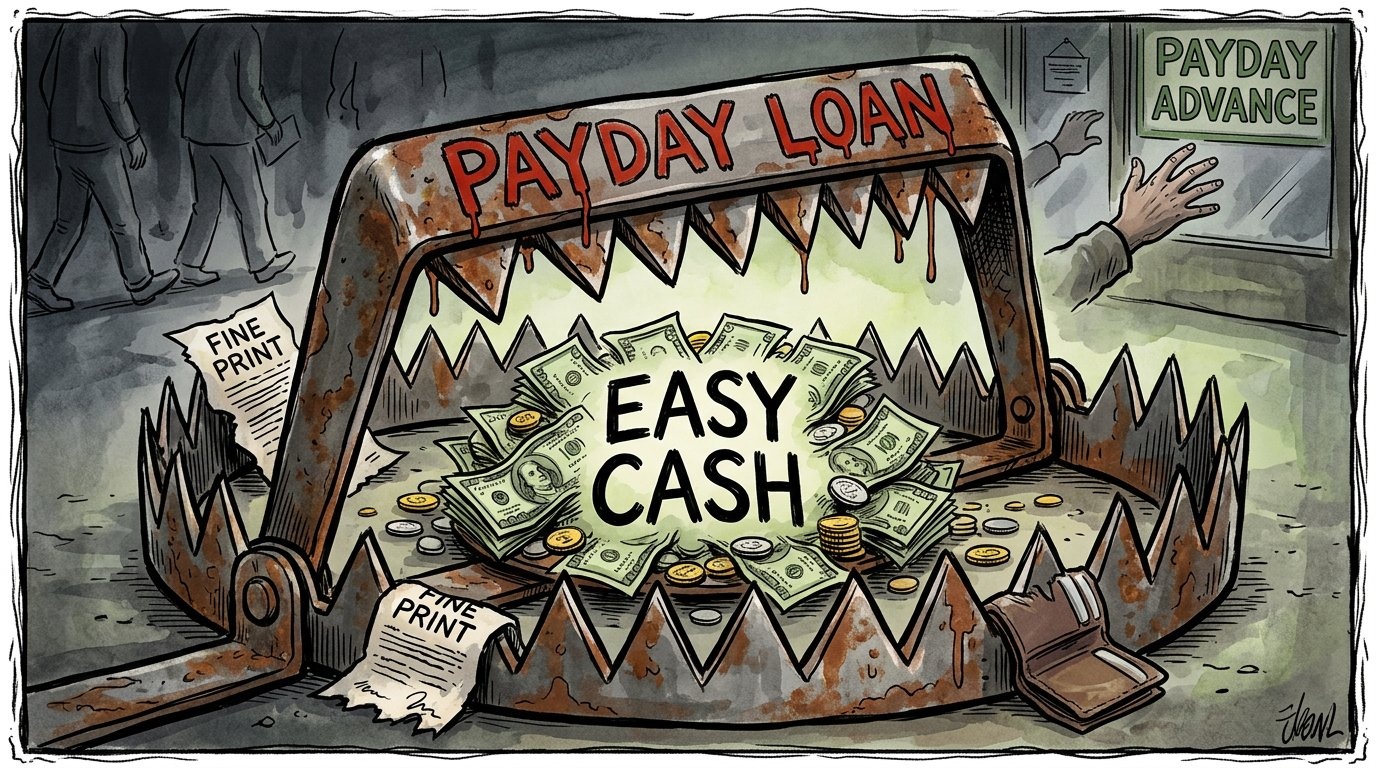

Here is how a payday loan works. You borrow, say, $400. You give the lender a postdated check or access to your bank account. On your next payday, the lender takes back the $400 plus a fee, usually $15 to $30 per $100 borrowed. That fee sounds small. As an annual interest rate, it works out to around 400 percent. A credit card, by comparison, runs about 20 to 25 percent.

The real trap is the rollover. If you needed the $400 on week one, you'll probably need it just as badly on week three. If you cannot pay on payday, the lender lets you "extend" the loan for another fee. About 80 percent of payday loans are followed by another loan within two weeks. That $400 can turn into $700 by the end of the month.

If money is tight, these options cost far less:

A Payday Alternative Loan (PAL) from a federal credit union. By law, the rate is capped at 28 percent. You can borrow $200 to $2,000 and pay it back over up to a year.

Earned wage access through your employer. Many companies now let workers tap pay they have already earned before payday, often free or for a small fee.

Call the biller. Utilities, hospitals, and landlords routinely offer payment plans if you ask.

A credit card cash advance. Expensive, but cheap compared to 400 percent.